Out with the old and in with the new? Some of Britain’s once loved cars are now nearing extinction – check out the top ten most endangered car species below.

Ford Cortina

The Ford Cortina has gone from being one of the most common to one of the rarest models on the roads. From 4,154,902 Cortinas (of all types) produced between 1962 and 1982, there are less than 3,000 remaining.

Ford Sierra

Notable for its trailblazing aerodynamic design, The Ford Sierra was the Ford Cortina’s replacement in 1982, with 3,470,524 manufactured. Of the much-revered vehicle’s total number, less than 3,000 remains.

Vauxhall Victor

Between 1957 and 1976, 827,159 Vauxhall Victors were manufactured. At one point, the Vauxhall Victor was Britain’s most exported car with sales in the many right-hand drive markets such as the USA and Sri Lanka. Today, less than 1,000 remain on the roads.

Austin Metro

The Austin Metro was manufactured between 1980 and 1998, going by a number of different names including the MG Metro and Rover Metro. Out of the 1,518,932 manufactured, under 500 are still registered.

Morris Marina

Despite its popularity and its global presence in the 1970s, the Morris Marina has been ranked as one of the worst cars ever built. This may explain why only 200 or so remain of the 809,612 manufactured between 1971 and 1980.

Hillman Avenger Tiger

The Hillman Avenger Tiger went by around a dozen or so monikers in its various forms around the world. Of the 638,631 originally made, around 200 are still in existence.

Vauxhall Chevette

The Vauxhall Chevette was a supermini car, made by Vauxhall between 1975 and 1984, the name Chevette intending to mean a small Chevrolet. Less than 200 models remain from the 416,058 initially created.

Austin Allegro

The Austin Allegro was produced between 1973 and 1982. Save for its Italian equivalent, the Innocenti Regent, the majority of Austin Allegro’s were sold at home in the UK. From the original 642,340 less than 200 remains.

Austin Maxi

The Austin Maxi was the first five-door hatchback to be fitted with a five-speed transmission (i.e. 5 gears and 1 reverse gear) in Britain. Between 1969 and 1981, 472,098 were built of which under 140 remains.

Morris Ital

The Morris Ital was the descendant of the Morris Marina and is currently the most endangered car in the UK. Out of 175,276 less than 30 exist today.

All vehicles that are registered in the UK and are driven or kept on public roads must be taxed. Car Tax is officially known as Vehicle Excise Duty (VED) and it is sometimes referred to as road tax, although this is not strictly the same thing. VED is handled by the DVLA (Driver and Vehicle Licensing Agency) who use the money they collect on car tax each year to make improvements to the roads.

As of April 2017, new car tax rules came into effect and as of April 2018, a new rule for diesel cars was also brought in. The most recent changes to car tax were announced in The Autumn Budget of 2018/2019, which states that car tax rates for cars, vans and motorcycles will go up in accordance with RPI (Retail Price Index) from April 1st 2019.

This means that there are three different tax systems currently in use, so which one you are subject to, will depend on when your car was first registered. It is important to remember that in the case of used cars, the date on which it was registered is not always the same as the date on which you bought it.

How Car tax is calculated

All cars belong to tax bands and tax rates are determined by:

Engine size

Fuel type

Carbon dioxide emissions

The cars first registration date.

Car Tax rates for cars prior to April 2017

Cars first registered before March 2001 are part of a fairly straightforward tax system that splits vehicles into two classes of engine size – those under and those above 1549cc. This is because official data about carbon dioxide emissions generally was not available at this time so engine size was the best way to calculate rates, which are:

1549cc or below – £155 per year

Above 1549cc – £255 per year

Cars first registered between 1 March 2001 and 31 March 2017are categorised by the volume of CO2 emissions they produce. Brand new cars are subject to what is known as the “showroom tax” in their first year, after which they will take on the standard rate, which are:

The Car Tax Rules as of 2017/2018

All cars that were bought brand new on or anytime after April 1st 2017 are subject to the following conditions:

Low-emission cars are no longer exempt from car tax

A standard rate of £140 is applied to call cars excluding those with zero co2 emissions, which pay £0.

Cars costing over £40,000 will have to pay an additional £310 per year over five years, after which they will pay the standard rate depending on what type of fuel it uses.

The first year rate is based on the amount of Co2 emissions produced by your car (as of April 2018, these rates have increased). From the second year, standard rates apply.

Diesel cars first registered after April 1st 2018 that does not comply with the RDE Act 2 emission testing must pay a higher amount of tax in the first year.

Owners of “alternative fuel” cars, such as hybrids, plug-in hybrids, biofuel, compressed natural gas or liquefied petroleum gas will pay £10 less than petrol and diesel owners in the first year, after which they will pay £130 every year.

Car Tax Band

CO2 Emissions

First Year Rate

Annual Rate After First Year

A

Up to 100 g/km

£0

£0

B

101 – 110 g/km

£0

£20

C

111 – 120 g/km

£0

£30

D

121 – 130 g/km

£0

£120

E

131 – 140 g/km

£130

£140

F

141 – 150 g/km

£145

£155

G

151 – 165 g/km

£185

£195

H

166 – 175 g/km

£300

£230

I

176 – 185 g/km

£355

£250

J

186 – 200 g/km

£500

£290

K

201 – 225 g/km

£650

£315

L

226 – 255 g/km

£885

£540

M

Over 225 g/km

£1120

£555

Statutory Off Road Notification (SORN)

If your car is off the road, or you plan to take it off the road, you will be required to officially declare your car’s status to the authorities, or you will need to continue paying car tax, car insurance and have a valid MOT. To do this, you must apply for a Statutory Off Road Notification (SORN).

Once you have declared your car off the road with a SORN, you will not be able to drive or park it on a public road. It will have to be kept on private land such as your driveway or in a garage. The only exception to this rule is that you are allowed to drive it to a pre-booked MOT and you must be able to prove this is where you are going, should you get stopped by the police.

If your car is not taxed or insured and you have not declared it with a SORN, you can be fined £80.

If you have any outstanding tax or insurance, you can apply t the DVLA for a refund for the remaining months of tax or insurance.

If you have a SORN and would like to get your car back on the road, you must have valid car tax, insurance and an MOT before you drive it. Once you apply for car tax, your SORN is automatically voided by the DVLA.

Selling or Buying A Vehicle

When vehicles transfer hands through buying and selling, Vehicle Excise Duty does not automatically transfer with it.

Even if the car you bought still has a number of months left on its tax period, you must apply for car tax, as the new owner, before you can drive it.

If you are selling your vehicle and you have one or a number of full months left on its tax period, you are eligible for a refund for that additional time. The DVLA will automatically issue this to you, once they receive the selling or transferring a vehicle section of your V5C (your vehicle registration document) from you.

Similarly, if you buy a car that has been declared as SORN by its previous owner, you will have to apply for a new SORN from the DVLA, if you plan to keep it off the road, as you are its new owner.

Misplacing important documents can be frustrating and stressful and unfortunately, it’s all too easy to do. However, if you know what to do and where to go, it’s just as easy to replace them! Below we will take you step by step through the process of replacing important motoring documents and certificates.

Driving License

Where:GOV.UK What: You will need to provide your Government Gateway ID (this is your user ID which can be obtained at the same time if you do not already have one) and details about where you have been living for the past 3 years. You shouldn’t need to provide a photograph, as it will already be on the DVLA system although you will be notified if you are required to provide a new one. Cost to replace: £20 How long it takes: 3 weeks Additional information: If you need to make changes to any of the details on your driving license such as if you have moved address, you will also be required to complete a D1 form which can be obtained from any branch of the Post Office. This will need to be posted along with payment to the address provided on the form.

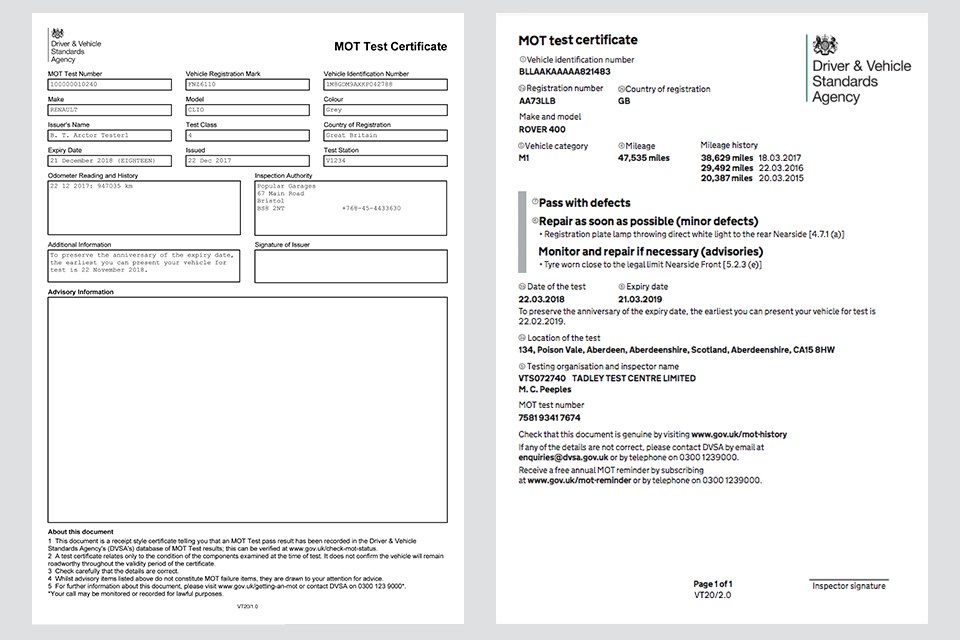

MOT Test Certificate

Where: Any MOT centre (it does not have to be the exact one that carried out the MOT). What:You will need to provide your vehicle registration and your V5C log book reference number. Cost to replace: A maximum of £10 How long it takes: Same day Additional information: You will receive a fixed penalty notice if your MOT is expired and you have been driving your car, however, it is fine to drive whilst waiting for a replacement certificate and your MOT is still valid. If the police stop you, they can check your MOT status via the Vehicle and Operator Services Agency database.

Log Book (V5C)

Where:You can apply for a new logbook via phone, post or at a Post Office. If your name, home address or vehicle details have changed you will have to apply via post. What:If applying via post, you will need to download and fill in an application form (V62) and send it to the DVLA along with the payment. Cost to replace:£25 How long it takes:Applications by phone will take up to 5 days to be processed whilst postal applications can take up to 6 weeks. Additional information: If you did not receive a V5C with your new car, you will need to apply for one by filling out the V62 and post it to the DVLA along with the green New Keepers Details part of your V5C that you were given when you bought the vehicle (if you don’t have this you will have to pay £25). This can take up to 6 weeks to process.

Ahead of the Ultra Low Emission Zone expansion in 2021, the Mayor of London, Sadiq Khan has announced plans for a £25million scrappage scheme, aimed at helping low income car owners switch to greener alternatives. This applies particularly to those that own older and especially diesel-fuelled vehicles.

What is the Ultra Low Emission Zone?

The Ultra Low Emission Zone in London will come into effect this April, replacing the 2017 Toxicity charge of £10 for cars built before 2005 driving in Central London. The new zone will initially encompass the existing congestion charge zone, however, it will be expanded in 2021 in order to incorporate the inner London area enclosed by the North and South Circular roads. The implementation of the Ultra Low Emission Zone will mean that diesel cars that do not meet Euro 6 emission standards and petrol cars that do not meet Euro 4 emission standards will have to pay a daily tariff of £12.50 to drive within the zone. It will operate all year long, 24 hours a day and will be added to the existing congestion charge. An estimated 2.5 million cars will be affected by the new charge once the zone has been expanded, however, it is anticipated to cut harmful emissions in the congestion charge zone by 45% by 2020.

Euro 6 Emission Standards: Your car was registered on or after 1st September 2015 / the model was approved on or after 1st September 2014.

Euro 4 Emission Standards: Your car was registered on or after 1st January 2006 / the model was approved on or after 1st January 2005.

London Scrappage Scheme

As part of the #LoveCleanAir campaign, city leaders are calling on the UK Government to set significant clean air objectives, proposing that the Government provides a £1.5 billion fund for a national vehicle upgrading scheme, in addition to making the World Health Organization suggested air pollution limits a legal requirement, to be achieved by 2030.

At the National Clean Air Summit last week, Sadiq Khan announced his plans to launch a £25million scheme aimed at helping businesses and residents of London scrap their older, more polluting vehicles in favour of more efficient alternatives.

Speaking on the impetuses for the scheme, the Mayor said, “Our country’s filthy air is a national disgrace that shortens lives, damages our lungs and severely impacts our NHS.”

The proposed £25million fund will be added onto the £23million being put towards a scheme launched in December 2018 that aims to incentivise businesses that operate in the ULEZ with ten or fewer employees, scrap their vans that do not meet the Euro 6 standards. This means that a total of £48million is going towards helping those that would otherwise be unable to afford it, upgrade to cleaner vehicles. This final budget will be presented to the London Assembly on 25th February and with approval, the scheme could be rolled out later this year.

Car Manufacturer scrappage schemes

A number of car manufacturers are also operating their own internal upgrade scheme to encourage customers to swap out their diesel cars for low emission alternatives. The car you are trading in must meet the Euro 1 – 4 emission standards. The following manufacturers are offering the following schemes:

Manufacturer

Offer

Trade in qualifications

Models eligible on offer

Hyundai

Up to £4000 off a new vehicle

Car must have been registered before 01/10/2011 and meet Euro 5 standards or less

i10 1.0; i20; ix20; i30; i30 N Line; i40; Tuscon; Santa Fe; Ioniq Hybrid; Kona

Kia

Up to £3000 off a new vehicle

Car must have been registered before 31/03/2012, and meet Euro 5 standards or less

Picanto; Stonic; Niro

Mazda

Up to £6000 off any Mazda model that emits less than 136g/km of CO2

Car must have been registered before 31/03/2012 and meet Euro 5 standards or less

motorly is a credit broker, not a lender. Rates start from 6.9% APR. The rate you are offered will depend on your individual circumstances. Representative Example: Borrowing £5,500 over 48 months with a representative APR of 22.9% the amount payable would be £287 a month, with a total cost of credit of £1406 and a total amount payable of £6906.

Toyota

Up to £2500 off a new vehicle

Car must be more than seven years old and you must have owned it for at minimum of 6 months.

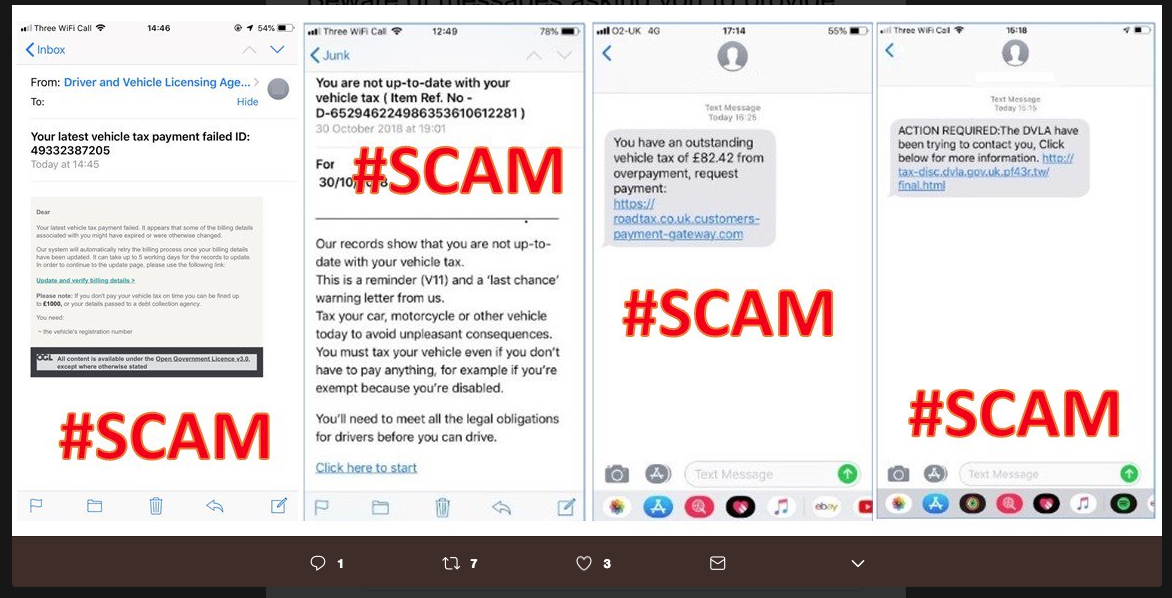

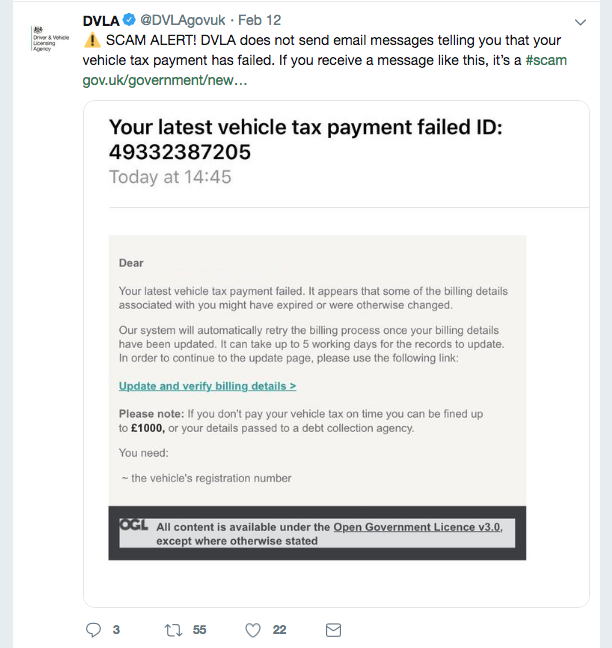

The Driver and Vehicle Licensing Agency have released a warning against new scam emails and text messages, impersonating the DVLA with the aim of eliciting bank details from motorists.

The messages being sent to motorists around the UK are designed to look like they are legitimate correspondence from the government organisation, notifying drivers that a vehicle tax payment has failed. The message explains that an invalid, expired or altered billing detail is the cause of the failed payment and that drivers could face a fine of up to £1,000 if vehicle tax payments are not made on time. The message also contains a hyperlink which leads the recipient to a false website where they are prompted to enter their bank details.

The DVLA shared an image of the fraudulent message on its social media profiles:

The DVLA has confirmed that this is not a genuine message and has not come from them. It has stated that it does not send out emails or text messages that ask customers to verify personal details or provide payment information and has advised anyone who receives this message to not click on any links and delete the email or text straight away.

In its official statement, the DVLA has also issued a general warning to customers about searching for the DVLA website through Google as there are a number of third-party websites falsely claiming to be the DVLA. These websites might be offering things like help with applying for a driving license or taxing your car. A tell-tale sign that you are being misled is if the website is asking for fees for services that can be obtained for free (or at a lower cost) on Gov.uk. Don’t be fooled by details such as having “dvla” in the website URL or the use of DVLA logos.

Recent studies have found that in 2018, motorists on the most congested roads in the UK spent an average of 178 hours stuck in traffic. That equates to about one week simply sat in traffic, costing the average driver approximately £1,317 each and the UK economy a total of £7.9 billion over the course of the year. Unsurprisingly, drivers in London spent the most time sitting in traffic queues, totting up an average of 227 each in 2018 (9.5 days), followed by Edinburgh (165 hours / 6.8 days) and then Manchester (156 hours / 6.5 days).

Globally, Britain is one of the worst places for traffic, with leading motoring associations concerned that it is only getting worse with time. In this article, we will explore some of the main causes of traffic jams in the UK as well as a couple of things that motorists can do to help ease congestion

Large scale problems that can cause traffic:

One of the most obvious causes is that the roads are simply over capacity with cars. Rising numbers of cars on the roads can in part be attributed to cars becoming much more affordable as a result of new finance options, global manufacturing and an increase in personal wealth overall. Whilst this in itself is not so much of a problem, the lack of infrastructure to cope with so many vehicles, coupled with uncontrollable factors like the weather and struggling, underfunded public transport systems has led to roads becoming too full up.

Another one that goes without saying is the weather. During adverse conditions like heavy rain, snow and low temperatures, people are more inclined to jump in their car rather than face the elements on their way to work meaning there are more cars on the roads than usual. What’s more, road conditions and visibility worsen significantly in bad weather meaning that the likelihood of accidents and mechanical failures goes way up. And when accidents or breakdowns do happen, traffic is an inevitable consequence due to part of the road becoming inaccessible – plus cars may need to slow down and move to the side for emergency vehicles in particularly bad incidents.

Mechanical failures and breakdowns can also be attributed to other factors too. If a person has neglected to maintain their car properly and suffers a fault in their engine or tyres, then they are more likely to break down whilst on the road. However, unpredictable things such as sharp objects and poorly maintained roads (e.g. potholes) also put drivers and their cars at risk of experiencing untimely mechanical failures and as a result, producing blockages in roads.

Poor, dangerous and competitive driving can also be partially to blame for traffic jams. Drivers that do not obey speed limits, those that drive under the influence of alcohol or drugs or those that are distracted by their phones, other passengers, food etc. put themselves and others at risk of an accident and therefore contribute to congestion.

Rubbernecking is one of the most preventable causes of congestion. This refers to the way in which cars will slow down when passing an accident in the opposite direction in order to take a look at what has happened. As naturally curious beings, we are all guilty of doing this when an incident has occurred on the road however it is a major cause of traffic jams. Not only does it slow down the flow of traffic, but it is also very dangerous as drivers become distracted, not focusing on other cars and the road around them, making the chances of another collision more likely.

Braking, although it sounds strange, is, in fact, one of the major causes of traffic and specifically what is referred to as “phantom” traffic jams. This refers to when congestion seems to be unexplained and not attributable to anything obvious like roadworks or an accident. The cause of it comes down to the simple act of braking which creates a chain reaction effect that travels down the line of cars. The theory goes that when one car touches their brakes even briefly and their brake lights are illuminated, the car behind will do the same in anticipation of going into the back of them. The car behind them and so on will do the same, with the brake pressing action lasting slightly longer each time which eventually leads to all cars coming to a halt. The same effect can also be created when one driver changes lanes suddenly and the cars in the receiving lane must brake to maintain a safe amount of space between them and the joining car.

Smaller scale and temporary factors that can cause traffic:

Smaller road/ utility works and repairs including the use of temporary traffic lights and sometimes road closures.

Double parking causing a bottleneck situation.

Traffic lights out of sync as a result of technical problems.

Too many pedestrians at a crossing preventing a car to turn.

Special events such as music concerts and sports games that see an increase in the flow of both cars and pedestrians.

Temporary disruptions to public transport services.

What can you do to help reduce traffic jams?

If all drivers made a handful of changes to help decrease congestion, then the overall problem could be reduced significantly. Some things that you can do include:

Plan an alternative route that tries to avoid roads where major congestion occurs. Consider taking a slightly longer route than usual as in the long run, this may actually save you more time during rush hour. There are a number of free traffic apps that use GPS to track traffic and provide real-time information about road closures, route planning and heavy congestion that can help with this.

Whilst it is not against the law to use your phone as a sat nav (as it is illegal to call or text when driving), having your phone visible and within reach is still very risky as it can still divert your attention away. Try to avoid looking at or reaching for your phone at all to minimise distraction. If you have to use it as a sat nav, familiarise yourself with your route beforehand so that you are not overly dependent on it whilst driving.

Distracted driving also includes things like eating, drinking and smoking, as well as adjusting the radio, having music on too loud and even other passengers. Be mindful of anything that causes you to become distracted from the road and fellow road users, and make efforts to minimise it.

Driving whilst tired is a common yet preventable cause of collisions. Ensure you are not drowsy driving by getting enough sleep the night before you are planning to drive. Things like alcohol, prescription medication and some over the counter medicines can also increase drowsiness, lower attentiveness and impair judgement. It goes without saying that you should never drive under the influence of alcohol but if you are on any medicines, be sure to check the side effects for drowsiness.

Aggressive and competitive driving is also a major source of congestion and unfortunately, it is a cyclical effect, with bad traffic causing people to become antagonistic and angry whilst trying to get to their destination. This kind of driving endangers yourself, your passengers and other road users, doing nothing to reduce congestion and only increases the likelihood of accidents.

When comparing insurance quotes, you’ll often be given the option to add on what is known as “ancillaries” that provide additional cover to the standard third-party/ comprehensive/ multi-car policy that you pick. These extras are both general and more specific so that you can pick and choose the types of cover that you think you could need, depending on your lifestyle, the kinds of journeys you make, where you leave your car parked at night etc. Below, we will outline what each extra is and what kinds of situations they cover:

Breakdown Cover

Having breakdown cover will guarantee that in the event of a breakdown, you will be able to get roadside assistance and not be stranded. Few insurers will include breakdown cover as part of their policies and so usually it will have to be added on or purchased separately from another provider – therefore it’s a good idea to have a look around for different deals before you add it on. You should also take into account that the level of breakdown cover provided will vary between insurance providers and so ensure that you are getting the right cover to suit your needs. Breakdown cover will usually fall into these categories:

Roadside assistance

Recovery/relay – if your car can’t be fixed at the roadside and needs to go to a garage.

Home start – if you break down at home.

Onward travel – if you breakdown far away from home and your car needs significant repairs, you may be given a replacement hire car, overnight accommodation or onward travel expenses.

European cover – when driving in Europe up to a limit of 31 days at a time and 90 days a year in total.

Windscreen Cover

Windscreen cover will allow you to recover the costs of any repairs to your windscreen as a result of chips or cracks, or even the cost of an entire windscreen replacement if necessary. Even though it is called “windscreen” cover, it will often cover any other windows in your car and sometimes sunroofs too. The majority of comprehensive car insurance policies will already include windscreen cover and you might have to pay an excess, although this will vary from policy to policy.

Legal Cover

Legal cover provides you with financial protection against any costs you may incur from making a claim against another driver, or another driver making a claim against you in the event of an accident. Legal cover might be included in some policies but not always and is usually capped at a value of £50,000 (although you should check this with your insurer). Legal Cover can provide protection against the following uninsured losses:

Loss of earnings,

Transport fees,

Personal injury,

The excess on your policy.

Driving abroad / Green card

Most UK car insurance policies will cover you by the minimum compulsory requirement for driving in any other EU countries although this usually won’t include things like theft and fire damage. With regards to Britain’s departure from the European Union this year, it is not yet known what effect this might have on car insurance policies covering UK motorists in Europe, so if you have a trip planned it is best to contact your insurer about any questions you have. It has been widely speculated that in the event of a no-deal, UK drivers will need to be in possession of a green card if they are going to be driving in the EU, which proves that your policy provides the minimum, third party cover. These are free to acquire, so it is worth getting one just in case. Read more about the effects of Brexit on the car industry and UK car drivers in our blog post here.

Personal Effects Cover

The majority of comprehensive policies will include cover for any personal belongings inside your vehicle that are damaged in an accident or stolen from your car. This kind of cover is much less common with third party, fire and theft policies. Depending on your insurer and the policy, the value of items that will be covered can vary anywhere between £50 and £500. Bear in mind that many insurers will include certain clauses that mean that you might not always be able to claim, such as there must be signs of forced entry and items must be stowed away in the glove box or boot, not left in plain view. Because there are a number of limits and exclusions on Personal Effects Cover for car insurance, many people will choose to cover their personal belongings through Home Contents insurance instead, which itself will have an option to cover personal possessions outside of the home (i.e. in your car).

When it comes to getting cover for your in-car stereo and sat nav equipment, most insurers will treat factory fitted systems differently to separately installed systems so you need to disclose this to them. Non-manufacturer equipment is usually considered to be a modification and therefore you may experience higher premiums as a result.

Lost/stolen keys

Replacement key cover is included as a standard part of some insurance policies but not all and the level of cover available will vary between policies and insurers. Most of the time you will not have to pay an excess when you make a claim for lost or stolen keys and it usually won’t affect your no claims bonus either. Usually, you will be able to recover any costs relating to lost, stolen or broken keys up to a value of £1500 and some policies will even cover the cost of a hire car and transference of your vehicle if you are left without your keys far away from home.

Uninsured driver protection

Uninsured Driver Protection will cover you in the event that you are in an accident with an uninsured driver so that you won’t have to pay an insurance excess, lose your no claims bonus and in some cases, pay for repairs to your car yourself. In order to claim, you will have to provide the details of the uninsured vehicle as well as adequate proof that the accident was not your fault.

Personal Accident Cover

Personal accident and injury cover on car insurance is in place to provide compensation in the event of death or significant injury as a result of being in a car accident when you are unable to claim from a third party. Each policy will specify the kinds of injuries that are covered and compensation is usually capped at a maximum of £5000. Various policies will also have certain clauses and exclusions, for example, sometimes only the driver and his/her spouse will be covered and some policies will even exclude older people over a certain age.

There are a variety of different extras on offer so it’s important to conduct thorough research before deciding whether to add any on. Some are more useful than others and it really depends on your specific requirements, i.e. there’s no need to add on European cover if you don’t plan to be driving abroad within the next year! On the other hand, breakdowns can happen to almost anybody at any time due to a number of various problems, so with extras like breakdown cover, it is definitely a case of being safe than sorry.

In the UK, it is a well-known fact that there is a pothole epidemic on our roads. A combination of traffic, wet weather and cold temperatures are the main cause of the craters on the tarmac, which means that the winter months are when potholes become worse and much more common. In last October’s budget, the government promised that £420million would be given to local councils in England to deal with “potholes, repair damaged roads, and invest in keeping bridges open and safe” however many are saying that this is not an adequate sum of money, with the estimated repair cost for all of the potholes in England, being well into the billions. To make matters worse, it is not just our roads that are being damaged; an estimated 1 in 10 mechanical faults in cars are caused by potholes and it is costing motorists around £730 million every year in repairs. In this article, we will be looking at:

What kind of problems potholes can cause your car

What you can do to minimise the damage

How to report a pothole and make a claim for damage as a result of a pothole.

What kind of problems can potholes cause your car?

Tyres

As the main point of contact between the road and your vehicle, your car’s tyres will take on much of the impact felt as your car drives over an uneven patch of the road. As your tyre enters into a pothole, the distribution of the car’s weight is shifted slightly and more pressure is placed onto the one tire that makes direct contact with the pothole. The same thing happens again when the tyre leaves the pothole and as the edge of the crater strikes your tyre on exit, the force can cause a rupture, bulges or bubbles, misshape your tyre or even cause the rims to bend. The depth and severity of the pothole as well as the angle and speed at which your car hits it, will all affect the degree of damage to your tyres. However, it goes without saying that the more times you drive over a pothole, the more likely you are to experience these problems.

Suspension and Wheel Alignment

Your car’s suspension is designed to absorb the impact of driving and increase the smoothness of your ride however potholes can cause your cars tracking to become disrupted and your wheels alignment to be knocked off kilter. The result of this can be uneven tyre wear, car drifting to one side, a skewed steering wheel and vibration or a screeching or squeaking noise coming from your tyres. What’s more, your car will become less fuel-efficient and you could end up paying more to get your tyres replaced more often. Correct wheel alignment is not only necessary for the condition of your tyres, but it is essential for safety on the roads – you do not want to be veering into oncoming traffic, experience a blowout in one of your tyres as you are driving along or be unable to move swiftly out of the way of an emergency.

Exhaust

In the majority of cars, exhaust pipes will run along the underside of the car putting them in prime position for contact with pothole edges. Particularly severe potholes can cause the undercarriage of your car to scrape along the tarmac, which can result in denting or holes in exhaust pipes, mufflers or catalytic converters. A hole in your cars exhausts system may produce noticeable noises, reduce the power of the car or even allow harmful exhaust fumes to enter into the cabin and expose you and your passengers to a dangerous health hazard. A damaged catalytic converter can also mean that your cars exhaust fumes have not been filtered properly and your car is pumping excessive amounts of harmful pollution into the atmosphere.

Body

Cars that are particularly low on the ground such as performance and sports cars are also at risk of experience body damage as a result of potholes. Low placed bumpers can scrape against pothole craters, paintwork can be scratched more easily and dents are another risk. Though this kind of damage won’t necessarily affect the safety or performance of your car, it can decrease the value of your vehicle as well as increase your cosmetic repair bill.

What you can do to minimise the damage:

With approximately one pothole for every one mile of road in the UK, it is impossible to completely avoid driving over them however there are a couple of things you can do to mitigate the impact on your car.

Be aware of potholes and slow down as you approach it – the faster you are driving when you hit one, the more damaging it will be to your vehicle.

Leave a good amount of space between you and the driver in front to give yourself time to react and prepare to slow down.

Puddles in the middle of the road are a sign of potholes, so drive through them with caution.

Do not brake as you hit a pothole as this can actually cause more damage.

Keep your tires properly inflated to the recommended pressure.

How to report a pothole and make a claim:

The first thing to do before you report or make a claim on pothole damage is to collect evidence of the pothole in question and the damage caused. The best kind of evidence is photographs, so ensure that you take pictures of the pothole from different angles and try to indicate the depth of it by including an object like the nearest lamppost or tree to show the scale. You should also take pictures of the damage to your vehicle. Note down the name of the road and whereabouts on the road the pothole is situated i.e. near to a junction.

Reporting a pothole is very simple as all councils in England have a service to report potholes on their website. To find out which council maintains the road with the pothole on, you can enter the road name, town or postcode into the Gov.uk website. If the pothole is on a motorway or major A-road, it is best to go directly to Highways England who is responsible for maintaining these roads.

Before making a claim, it is important to bear in mind that your chances of success are reliant on whether the council is already aware of the pothole in question, i.e. if it has already been reported to them. If the pothole has not been reported, councils are likely to argue that they cannot be held responsible for a pothole that they are not aware of. Therefore, you should always report a pothole if you come across one.

If your car needs to be repaired as a result of the damage caused by a pothole, get some quotes and keep all quotes, invoices and payment receipts safe. It is also a good idea to make copies of them to include in your claim.

Next, you should write to the relevant authorities, either the council responsible for the road or Highways England, outlining the reason for your claim, what occurred, the damage incurred to your vehicle and all evidence including photographs, quotes, invoices and receipts. If the authority believes that you have a valid claim, they will usually send you a damage report form that you will be required to fill out and send back. In addition to the form and your own evidence, you could also be asked to provide quotes and invoices of the repairs, an up to date MOT certificate and photos of the damage.

Remember that if the relevant authority has not previously recorded the pothole, and they can prove that they have a regular inspection and repair system for roads in place, your chances of making a successful claim are slim and so you should prepare yourself for this possibility. If your claim is rejected, it might be worth going to the small claims court, although bear in mind that you could end up with additional legal costs by doing this so it is important to weigh up the various costs against what there is to gain.

What are smart motorways?

A smart motorway is an area of motorway that is controlled by active traffic management (ATM) technology that aims to reduce congestion and increase motorway capacity in particularly busy areas. They can be identified by the absence of a hard shoulder, as well as variable speed limits and other information displayed on digital screens on the gantries overhead. There are three main types of smart motorway:

Controlled Motorway (CM)

Controlled motorways maintain the traditional layout of three or more lanes with a hard shoulder, which should only be used in the case of a genuine emergency.

The mandatory speed limit is also displayed on the overhead signs, although it is subject to change depending on the traffic conditions. Therefore, drivers must be mindful and responsive to any speed limit changes at all times. If there is no speed limit displayed, then the national limit applies. CCTV and speed cameras are used along smart motorways to enforce speed limits. Highways England has confirmed that the speed cameras are deliberately updated with the new speed limit slightly after drivers are, in order to allow people to slow down safely without slamming on the brakes to slow down in time.

All Lanes Running (ALR)

An all lanes running scheme entails the use of the hard shoulder as an additional lane for cars to use normally. The only time the hard shoulder (or ‘first lane’) is closed off is when there has been an incident in which case, a red ‘X’ is displayed on the gantry sign overhead indicating that all vehicles must move out of that lane immediately. Failure to do is extremely dangerous and can result in points on your license and a fine.

All lane running motorways have Emergency Refuge Areas (ERAs) at the side of the road in the event of an emergency, that are spaced approximately 1.5 miles apart.

Like a Controlled Motorway, variable mandatory speed limits are displayed overhead.

Dynamic Hard Shoulder (DHS)

Dynamic hard shoulder running schemes make use of the hard shoulder as a normal running lane during particularly busy times but in normal circumstances, keeps it reserved for emergencies and incidents. A single white line is used to distinguish the hard shoulder from the carriageway and overhead signs will indicate whether it is open for normal traffic to use.

Like the other two types of smart motorway, variable speed limits are displayed overhead, speed cameras are in use and a red ‘X’ means that that lane is shut to normal traffic.

How much safer are smart motorways?

Smart motorways have received a mixture of responses since the very first one was implemented on the M42 in the West Midlands in 2006. Whilst their main purpose is to control traffic, improve the flow of vehicles and overall road safety, many people have said that the absence of a hard should actually makes them much more dangerous, particularly in the event of an emergency. In response to the criticism, Highways England has asserted that smart motorways have

Improved journey reliability by 22%

Reduced the number of personal injury accidents by over 50%

Severity of accidents when they did occur is much reduced with no fatalities and fewer serious injuries.

The future of smart motorways

Smart motorways are still being developed all the time, as constant advancements in technology enable improvements to the once basic system to be made. One major plan involves the use of sophisticated 5G broadband that will run through fibre optic cables along busy motorways between major cities such as London, Bristol, Leeds and Manchester. This 5G broadband will send real-time traffic updates straight to driver’s phones, including information about road diversions, heavy congestion and any accidents causing obstructions. There are even suggestions that this technology will be able to ‘predict’ heavy traffic and provide alternative route suggestions in real time (although to what degree it will accurately be able to do this is yet to be determined).

There are some plans to bring in drones on smart motorways, which could help to detect and send information about heavy traffic and potholes to the National Roads Telecommunications Service.

In Merseyside, an initiative involving smart LED road studs has already been implemented at one of the country’s busiest and most dangerous motorway junctions. Like normal cat eyes but with smart technology, these studs are synchronised with the nearest traffic lights and will turn off when the lights turn red, indicating for vehicles to prepare to stop.

All the smart motorways currently operating in the UK are as follows: